Token Issuance & AMM Liquidity

Understand how tokens get liquidity on the XRP Ledger — fungible tokens and trust lines, the order book versus the Automated Market Maker, and how an AMM prices trades. You build it in the assignments.

What you'll learn

- Enable rippling on an issuer account and explain why a token needs it.

- Create a trust line from a holder and issue a fungible token to it with a Payment.

- Reason about XRPL currency codes (3-char vs 40-char hex) and the trust-limit model.

- Spin up an XRP/token AMM pool with AMMCreate and read its state back.

- Explain the constant-product formula, trading fees, and impermanent loss for your pool.

Overview

You've moved XRP, the ledger's native asset. But most assets on the XRP Ledger are tokens — and a token nobody can trade isn't worth much. This lesson is about liquidity: how a token gets a market on the XRPL, and especially how the ledger's native Automated Market Maker (AMM) works.

No code here — this is the concept. You'll build it for real in the assignment.

Tokens on the XRPL

A fungible token on the XRPL is an IOU: a balance an issuer owes a holder. Every token is identified by its currency code plus the issuer's address, so USD from one issuer is a completely different asset than USD from another. Stablecoins are simply fungible tokens designed to track the price of an underlying asset.

A holder only receives a token it has agreed to hold, by opening a trust line — the ledger's built-in opt-in that keeps unwanted tokens off your account.

Two ways to provide liquidity

Once a token exists, the XRPL gives it two native places to trade.

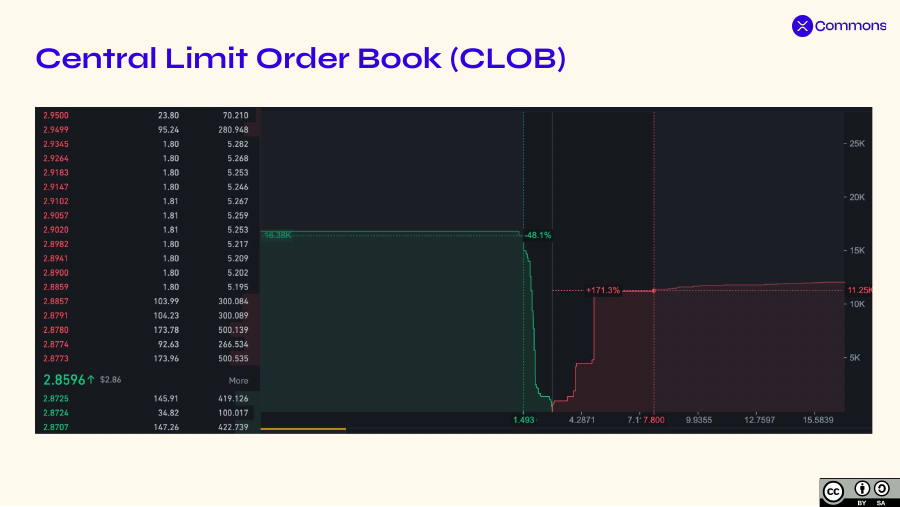

The order book (CLOB)

The Central Limit Order Book is the classic exchange model, built into the ledger: buyers and sellers post resting offers, and the ledger matches them by price and time priority. Its weakness is liquidity — a brand-new token has no offers to trade against, and keeping a book tight needs professional market makers continuously posting on both sides. With no one doing that, the book is empty: you can list a token, but you can't actually trade it.

The AMM

The Automated Market Maker is the answer to the empty book. Instead of waiting for someone to post an offer at the price you want, you trade against a pool of two assets, and a formula prices every trade automatically. Liquidity is always there — exactly what a thin, new market needs. And the two venues aren't either/or: when you trade, the ledger automatically routes your order to whichever — book or pool — gives the better price.

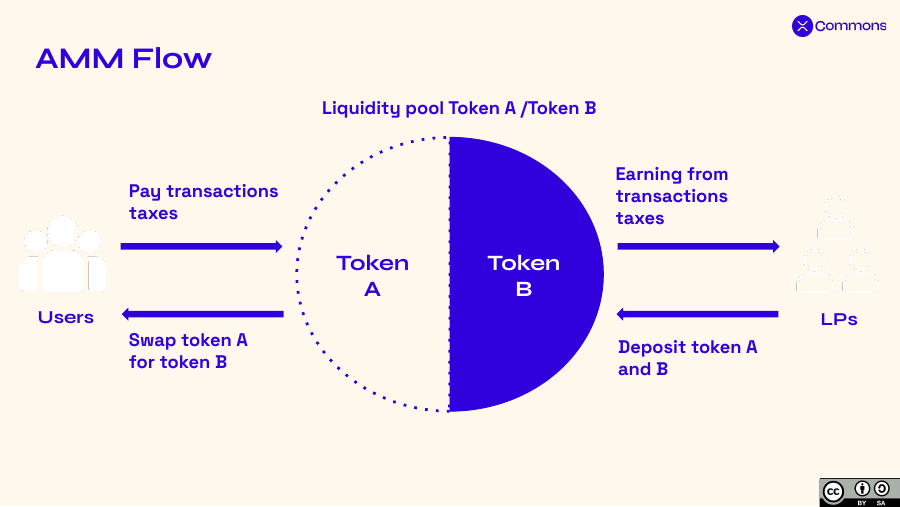

What is an AMM?

An AMM has two roles. Liquidity providers deposit both assets into a pool and earn a share of the trading fees. Users swap one asset for the other and pay those fees.

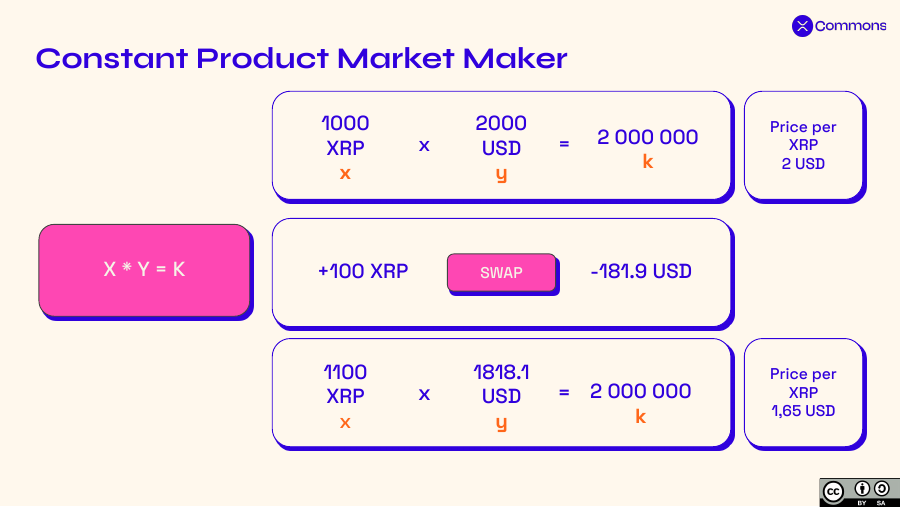

The pool prices trades with the constant-product formula: x × y = k. The two pool balances multiply to a constant k that every swap must preserve. So when a trader puts one asset in, the pool gives the other out until k holds again — and that moves the price. Big trades relative to the pool size move it more: that's slippage, and it's why deeper pools quote better prices.

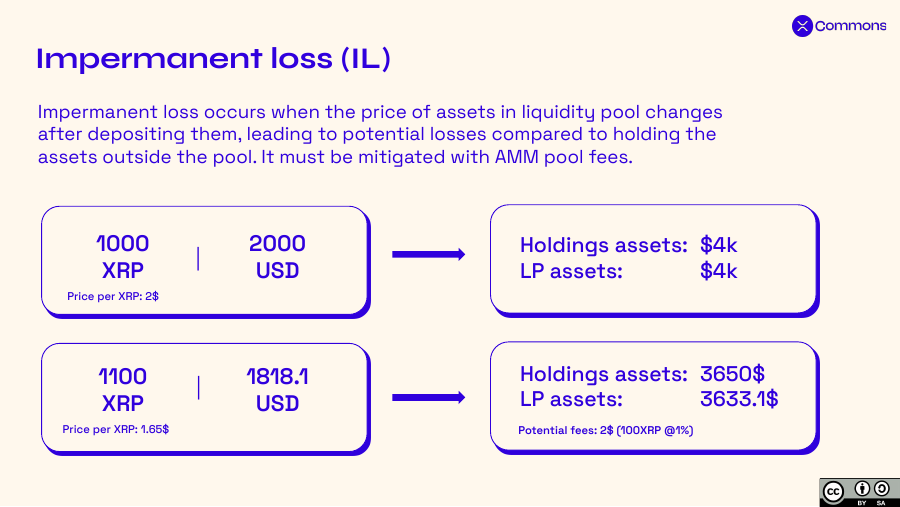

That same curve creates impermanent loss: if the price moves after you deposit, your pooled assets are worth a little less than if you'd just held them. The trading fees you earn are what offset it, and the loss reverses if the price returns to where you started. It's the key trade-off to understand before providing liquidity with real value.

The XRPL's AMM is protocol-native (no smart contract to deploy or audit), supports single-sided deposits, and its deterministic transaction ordering sidesteps the front-running common on other chains.

The steps

In the assignment you'll do this end to end. At a high level it's three moves and a handful of transactions:

- Create a token — enable rippling on the issuer, open a trust line from the holder, then issue the token with a payment.

- Create an AMM — pair your token with XRP in a new pool and set a trading fee.

- Swap — trade against the pool and watch the price move.

No exchange listing, no contract to deploy.

Check

You're done when you can explain, in a sentence each: what a fungible token is on the XRPL, why a fresh token's order book is empty, what an AMM does, and how a swap moves its price. Then head to the assignment to build it for real.

Resources

Assignments

0 of 4 completeAppears in