Introduction to the XRP Ledger

History of the XRP Ledger, how it works, accounts, tokens, the built-in DEX, and the XRPL consensus protocol.

What you'll learn

- Explain what the XRP Ledger is, why it was built in 2012, and what makes it purpose-built for payments.

- Describe the account and reserve model, and activate your own account using the testnet faucet.

- Distinguish native XRP from issued tokens (IOUs) held over trust lines.

- Explain what the built-in decentralized exchange does, including auto-bridging and pathfinding.

- Explain how the XRP Ledger Consensus Protocol reaches agreement without mining, in a few seconds.

Overview

You've seen what a blockchain is in general: an immutable, distributed ledger that lets parties who don't trust each other agree on a shared history. This module is about one specific ledger — the XRP Ledger (XRPL), the chain you'll build on for the rest of this track.

The XRPL isn't a general-purpose "world computer" that happens to do payments. It was designed, from day one, around moving value: sending money, issuing currencies, and trading assets, all settled in a few seconds for a fraction of a cent. That focus is why so much of what you'd normally bolt on with smart contracts — a token standard, an exchange, escrow — is already built into the protocol.

By the end of this module you'll understand where the XRPL came from, how accounts and reserves work, the difference between native XRP and issued tokens, what the ledger's built-in exchange does, and how the network agrees on a new ledger every few seconds without mining.

A short history: built for payments

By 2012, blockchains had proven that strangers could share a tamper-proof ledger — but the first generation was awkward for everyday money: proof-of-work burns enormous energy and takes minutes to settle a payment with confidence. The XRP Ledger launched in 2012 to fix exactly those limitations of crypto and traditional fiat rails, specifically for financial use cases, above all payments.

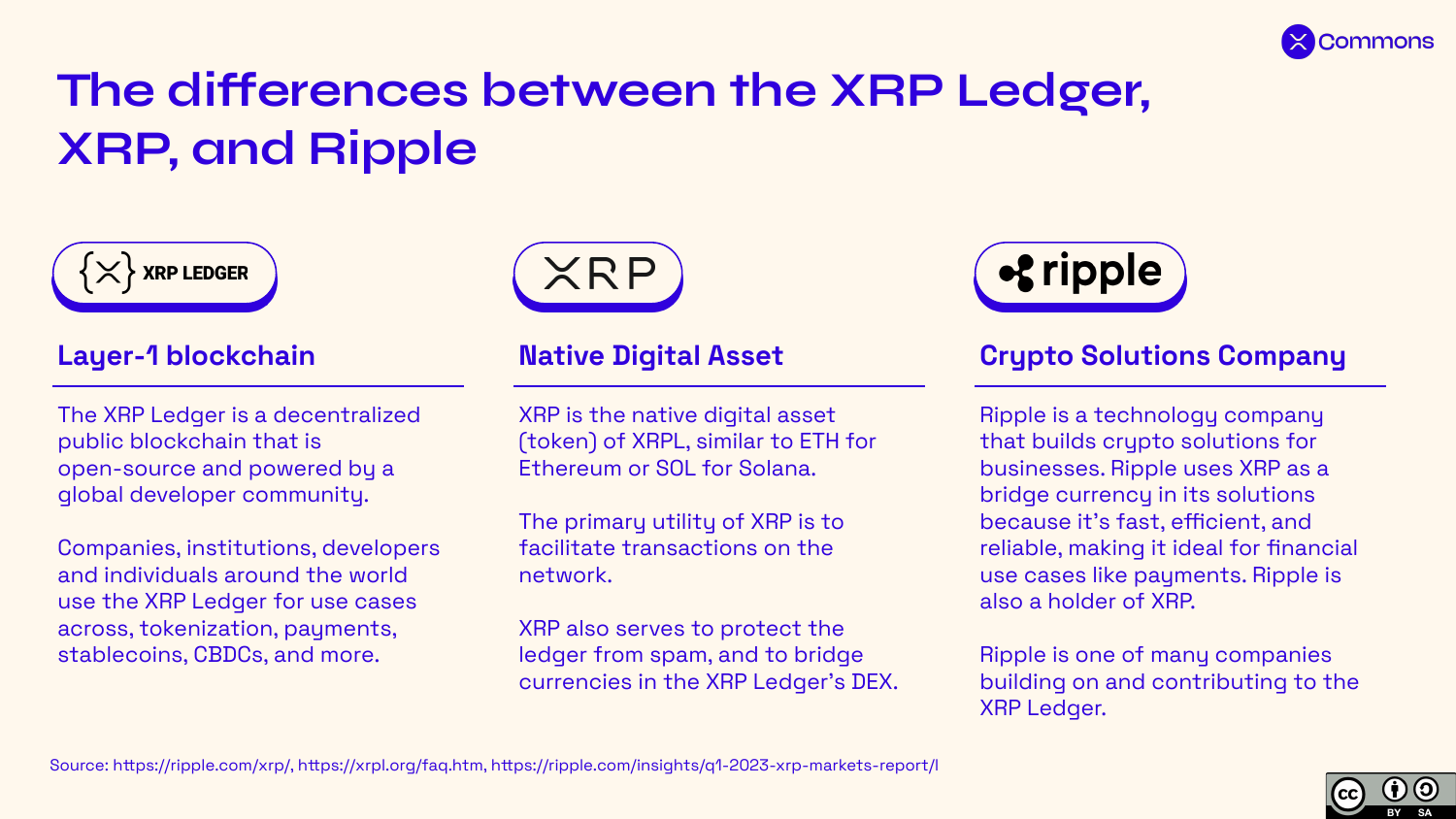

Three names get tangled together, so keep them distinct:

- The XRP Ledger (XRPL) is the Layer-1 blockchain itself — open-source, decentralized, maintained by a global community.

- XRP is the ledger's native asset, the way ETH is native to Ethereum. It pays transaction fees, deters spam, and acts as a bridge currency inside the exchange.

- Ripple is a company that builds payment products on top of the XRPL. It's one of many contributors — not the ledger, and not its owner.

The ledger has run continuously since 2012 without a failure or breach, settling billions of transactions — proof in production that a payments-first design can be both fast and durable.

The account and reserve model

To do anything on the XRPL you need an account, identified by an address (a string starting with r, like rPT1S...). Under the hood an account is the public half of a key pair: your public key is your address, your private key is your authority to sign.

One twist surprises newcomers: an address doesn't exist on the ledger until it's funded. To stop the shared database from filling with empty accounts, the XRPL makes every account hold a small amount of XRP it can't spend away — the reserve. On Mainnet today that's a base reserve of 1 XRP to keep the account alive, plus an owner reserve of 0.2 XRP per object the account owns (a trust line, an escrow, an offer, an NFT). The reserve isn't a fee paid to anyone — it stays in your account, simply locked while you hold those objects and released when you remove them.

The practical consequence: you create an account by sending it enough XRP to meet the reserve — there's no separate "register" step. It's also why your spendable balance is never quite your whole balance.

Native XRP vs issued tokens

XRP is the one asset native to the ledger — tracked directly in every account's balance, holdable without anyone's permission. But the XRPL is also built to carry issued tokens (often called IOUs): currencies, stablecoins, reward points, any asset an account chooses to issue. A token always has an issuer (the account that created it) and a currency code (like USD or EUR).

Because an issued token is a claim against its issuer, you can't receive one from just anyone — that would let strangers spam your account with worthless tokens. You opt in by creating a trust line: a ledger object saying "I'm willing to hold up to this much of this currency from this issuer." It records your balance with the issuer and caps your exposure.

The mental model:

- XRP = cash in your own pocket. Universally accepted, owes nothing to anyone.

- An issued token = a balance with a specific counterparty you've chosen to trust, up to a limit you set.

This split lets one ledger move both its native asset and a whole economy of issued currencies — the foundation for the exchange you'll meet next.

The built-in decentralized exchange

Here's where the payments focus really shows. On most chains, trading one asset for another means deploying or calling a separate exchange contract. On the XRPL the decentralized exchange (DEX) is part of the protocol — the first on-chain DEX in the world, live since the ledger's early days. Any account can place an offer to trade one currency for another, and those offers rest in a single shared order book the whole network sees.

Two features make this more than a basic order book:

- Auto-bridging. When two tokens have thin direct liquidity, the ledger can route through XRP as an intermediary (A → XRP → B) to find a better price — one of XRP's core jobs as a neutral bridge.

- Pathfinding. When no direct trade exists, the ledger assembles a path — a chain of hops across currencies and issuers — so the sender can pay in one asset and the receiver be paid in another.

Liquidity is consolidated in this one exchange rather than scattered across competing contracts, which tends to mean tighter prices. And because validators set transaction ordering rather than miners bidding for block space, the XRPL has no miner-extractable value (MEV) and front-running is extremely hard. The ledger also has a native Automated Market Maker (AMM) — liquidity pools alongside the order book, with the protocol picking whichever gives the better price.

Consensus without mining

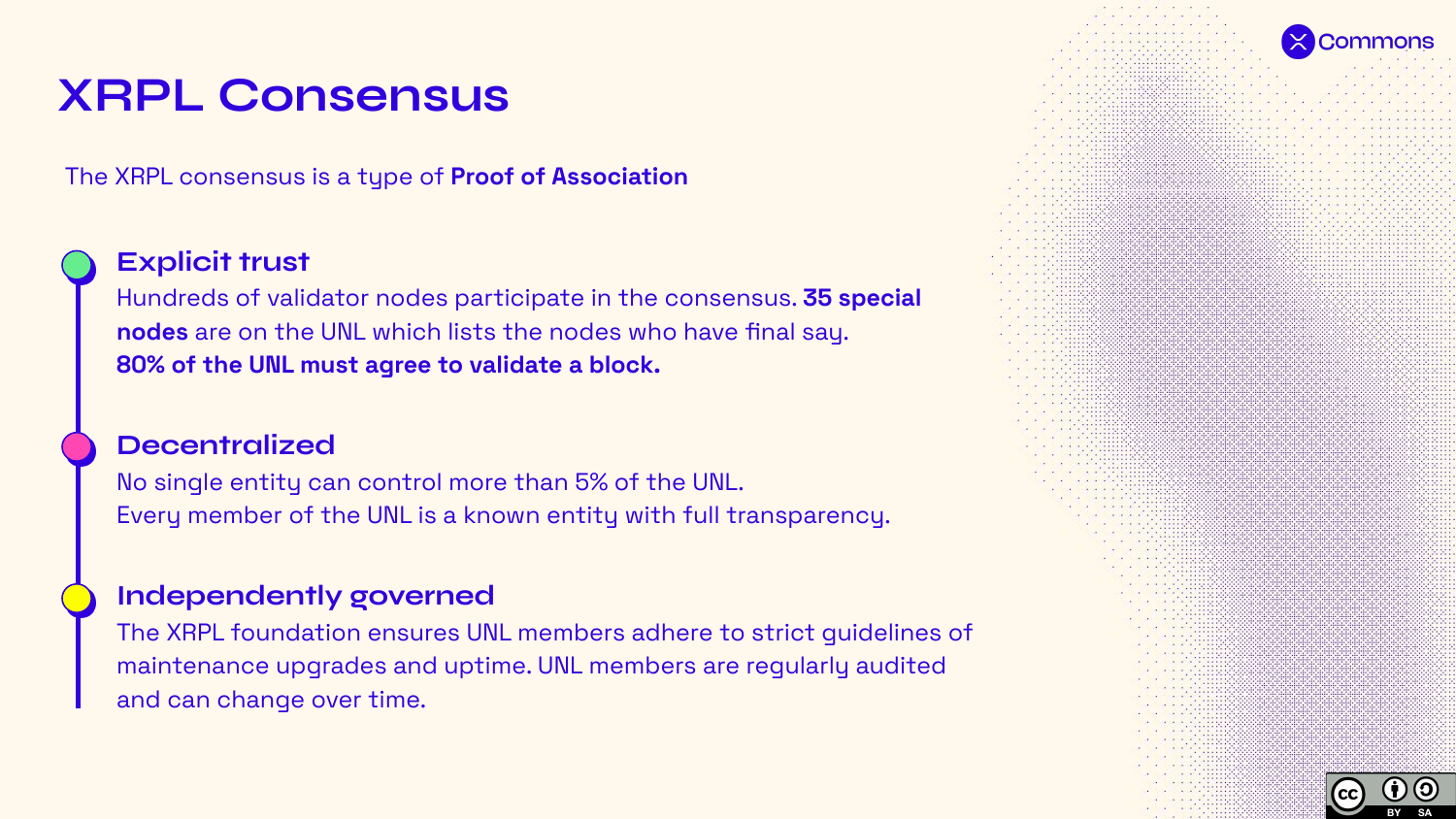

So how does the network agree on a new ledger every few seconds without mining? The XRPL uses the XRP Ledger Consensus Protocol, whose core idea is the opposite of an anonymous mining race: agreement comes from a set of known, trusted validators.

Each server keeps a Unique Node List (UNL) — the validators it trusts not to collude. Each round, validators propose the transactions they think belong in the next ledger and compare proposals over several quick passes until a strong supermajority agrees. The bar is high: more than 80% of trusted validators would have to collude to confirm an invalid transaction, and the network keeps progressing as long as fewer than 20% are faulty. Validators are run by a diverse, transparent set of universities, exchanges, businesses, and individuals.

The payoffs are exactly what a payments network wants:

- No mining — no electricity burned in a competitive race, so a very low carbon footprint.

- Fast finality — a ledger closes every 3–5 seconds, and once validated the result is final, with no waiting for confirmations to pile up.

- Low cost — fees are a tiny fraction of a cent, paid in XRP mainly to deter spam.

Every transaction you submit for the rest of this track rides this same protocol.

Resources

Assignments

0 of 2 completeAppears in